It is beginning to look like chip maker Intel hit the bottom in its products and foundry businesses in the second quarter of this year and that revenues are slowly – we won’t go so far as to say surely – improving. But now the restructuring charges and cost cutting is going to start to bite and the bottom line will look a little ugly for a while.

Then, Intel will run out of excuses, and hopefully in time for its 18A manufacturing process to catch a little fire among others designing chips for myriad purposes and for 18A processes to be brought to bear on Intel homegrown client and server products. In other words, 2025 should be a hell of a lot better than the misery that 2023 and 2024 was.

“Operationally, Q3 results exceeded our expectations as we achieved key milestones across Intel Foundry and Intel Products,” explained Intel chief executive officer Pat Gelsinger on a call with Wall Street analysts going over the numbers. “Underlying trends in the business are improving at a measured pace and our outlook for Q4 is modestly above current consensus. Overall, our stepped up focus on efficiency and execution across business is having a positive impact. We have a lot more ahead and we are acting with urgency to deliver on our priorities. We need to fight for every inch and execute better than ever before, and our teams are embracing this mindset as we build a leaner, more profitable Intel.”

In the quarter, Intel had revenues of $13.28 billion, down 6.2 percent year on year, and posted an operating loss across all of its groups and units of $4.6 billion, a stark contrast to the $8 million loss Intel had in the year ago period. And adding in another $5.62 billion in restructuring and other charges – a lot of this relating to laying off more than 15 percent of the Intel workforce ($2.2 billion), goodwill impairments for the Mobileye unit ($2.6 billion), and also writing down investments in gear used to make chips with the Intel 7 process ($3 billion), which etches at a 10 nanometer-ish geometries and which cannot be moved forward to support extreme ultraviolet lithography at smaller transistor geometries. Oddly, Intel also booked a $7.9 billion provision for taxes, pushing the company to a mind-numbing net loss of just a tad under $17 billion.

Ouch.

Operating income, by the way, was impacted by a $300 million write down of accelerator inventory – which we presume was for Gaudi 2 and Gaudi 3 devices, but also possibly for some “Ponte Vecchio” Max Series GPUs that Intel might have had laying around, “due to reduced revenue expectations.”

Gelsinger said on the call that “overall uptake of Gaudi has been slower than we anticipated as adoption rates were impacted by the product transition from Gaudi 2 to Gaudi 3 and software ease of use.” And to that end, Intel’s projections of bringing in $500 million for Gaudi accelerator sales (mostly for Gaudi 3 devices we presume) in 2024 will not be realized. With a $300 million writeoff, that seems to imply that Intel is only selling $200 million in Gaudi 3 gear. That implies that of the 32,000 Gaudi 3 accelerators that Intel thought it could sell in 2024, only 12,800 found homes. If you want Gaudi 3 accelerators on the cheap, Intel has 19,200 of them sitting around. That’s a little bit more than 40 exaflops at BF16 floating point precision, which would be a not too shabby cluster by any standard. However, you are going to have a lot of work to do with the software stack, and the Intel people who might help you might no longer work there.

So far, Intel seems to be sticking to its plan to evolve the Gaudi line into the “Falcon Shores” hybrid of its Ponte Vecchio/Rialto Bridge GPU and Gaudi 3 designs and iterated forward one or two notches. It would be a very bad thing if Intel gave up on AI acceleration, even if it does cost money in the short term. The AI server market is not going away, and as we have shown in many forecasts, it will eventually represent half or more of AI server spending. Intel cannot afford to leave all of that market on the table, even if it has to become a world class foundry again.

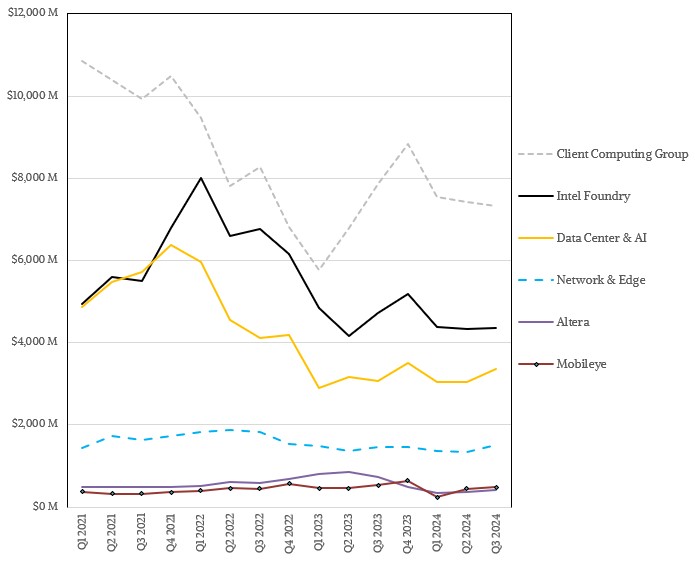

By the end of the decade, Intel wants that foundry to be driving $15 billion a year in external revenues, which is a little bit less that the Intel Products group pays Intel Foundry for etching and packaging today. Hopefully, when Intel Foundry is driving in excess of $30 billion a year in revenues – and possibly more – it will actually be a profitable business. Which it most certainly is not today, as you can see in the table below:

The main thing you need to be happy about in this table is that the Client Computing Group, which makes CPUs and GPUs for PCs, is holding its ground and represents the bulk of the free cash that Intel is generating. This is the fuel that will help Intel push through this terrible time.

If Intel had started on a genuine datacenter GPU business back in 2012, when it was very obvious that it would need one, and delivered on its potential, the Data Center & AI group would not be looking so rough right now. As it is, DCAI brought in $3.35 billion in sales, up 8.9 percent year on year and up 10 percent sequentially thanks to the ramp of the Xeon 6 server CPU lineup. With only $347 million in operating profit, which was reduced presumably by that $300 million writedown presumably related to the Gaudi accelerators not selling like hotcakes, operating income was down 11.3 percent but up 25.7 percent sequentially.

We are a long way from the close to 50 percent operating margins that the old Intel Data Center Group used to rake in.

Still, as this chart shows using the new groups that Intel set up in 2022 to describe itself to Wall Street (and that we extended backwards into 2021), things have stopped getting worse, more or less, and that is something. This is the only reason we can think of that Intel’s stock should have gone up in aftermarket trading in the wake of the report to Wall Street.

As you are well aware, we like to show the trend lines of Intel’s “real” datacenter business over time, which has become a lot simpler with the shutting down or selling off of its various network switch businesses (Barefoot Networks and Omni-Path) and the spinout of its flash storage business.

As best as we can figure from our model, Intel’s real datacenter business is 5/9ths are large as it used to be and only nominally profitable. Provided there are not any surprise writeoffs and charges going forward, this datacenter business, which includes all of DCAI plus slices of Altera and NEX at this point and is a lot less complex, should grow as Intel’s 18A processes are used for future “Diamond Rapids” P-core and “Clearwater Forest” E-core Xeon 7 processors. Gelsinger said that Clearwater Forest has powered on, and Diamond Rapids is shortly going into the fab for etching.